We already know that shopping habits changed dramatically at the start of Lockdown 1. The streets were quiet and shoppers stocked up in order to stay at home. People bought their food in fewer shopping trips than before – so, basket size went up but footfall went down. The average convenience basket spend in March 2019 was around £6.50, by 30th March 2020, the average basket value was £10.07! The items bought were influenced by the need to stay home – people were stocking up with items with longer shelf life. We saw items like pasta, rice and dried foods, tinned food like soup, flour for all the newly inspired home bakers, and of course toilet rolls, in high demand.

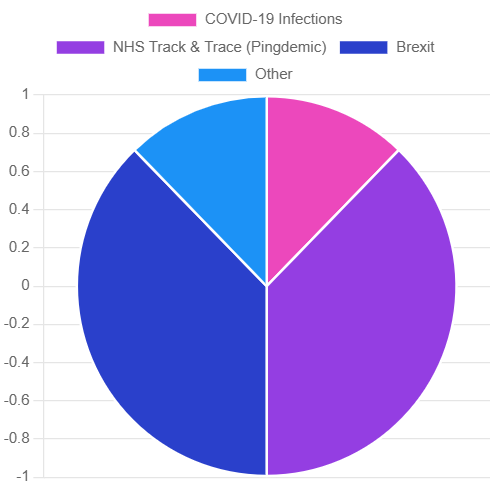

What has been the biggest impact for you?

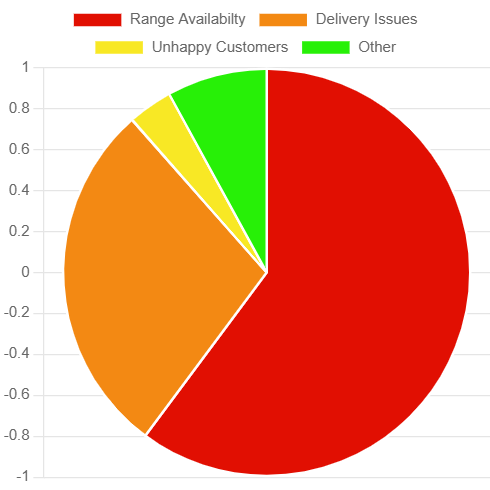

What do you think is most responsible for causing the supply issues?

The charts include stores throughout the UK, lockdown dates weren’t the same for Scotland, Wales and England (and we know there were actually official lockdowns in England). In the charts, we have shown the areas where we can see the biggest comparison between lockdown dates.

Of course, the impact of the lockdown wasn’t the same for all stores at he impact of the lockdown wasn’t the same for all stores , those in transient locations, who lost their footfall because workers stayed home, fared much worse than those in residential locations. In May 2020 the Prime Minister announced a conditional plan for lifting lockdown and shopping habits were adjusted accordingly.

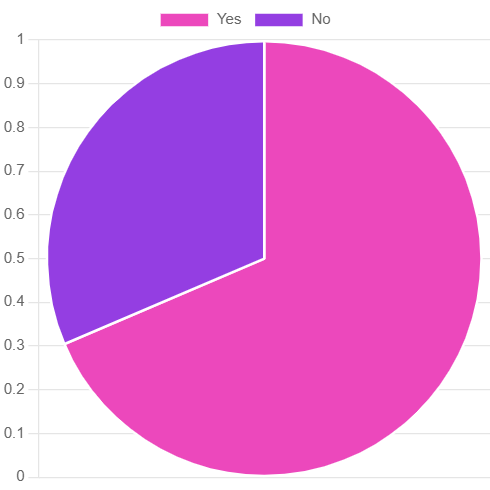

Have you been impacted financially by supply issues?

Basket spend reduced, but not down to 2019 levels. Footfall also began to rise slowly as workers who couldn’t work from home returned to the workplace and overall confidence increased. On September 30th, the government said it wouldn’t hesitate to impose further restriction if needed. This prompted a second panic for some shoppers, widely reported in the media. In 2021 we saw the same effect as before, but to a lesser extent, reduced footfall and larger spend per basket. In this Lockdown we saw increased sales of toilet rolls and baby wipes. Tinned food was also back in high demand. There was a cautious lifting of restrictions around Christmas, families juggled their changed celebratory plans and most of us stayed home rather than visiting families. On 2nd December we returned to a 3-Tier system which was upgraded to a stricter, 4-Tier system on 19th December.

On January 4th, Scotland entered lockdown again, and on 6th, England entered its third official full lockdown – schools were closed once more. Shoppers had adjusted and though basket size stayed high, we didn’t see a repeat panic purchasing or store shortages. Finally, on 8th March, the schools reopened and we see a slight fall in basket spend, possibly as students make the most of their ability to spend pocket money after school.

Shopkeepers and business owners everywhere keep their (sanitised) fingers crossed that the new normal becomes a permanent normal and the UK sees no further lockdowns.